The SSBJ issues Exposure Drafts of Sustainability Disclosure Standards to be applied in Japan

The SSBJ issues Exposure Drafts of Sustainability Disclosure Standards to be applied in Japan

The Sustainability Standards Board of Japan (“the SSBJ”) was established in July 2022 to develop Sustainability Disclosure Standards to be applied in Japan and to contribute to the development of international sustainability disclosure standards, following the establishment of the International Sustainability Standards Board (ISSB).

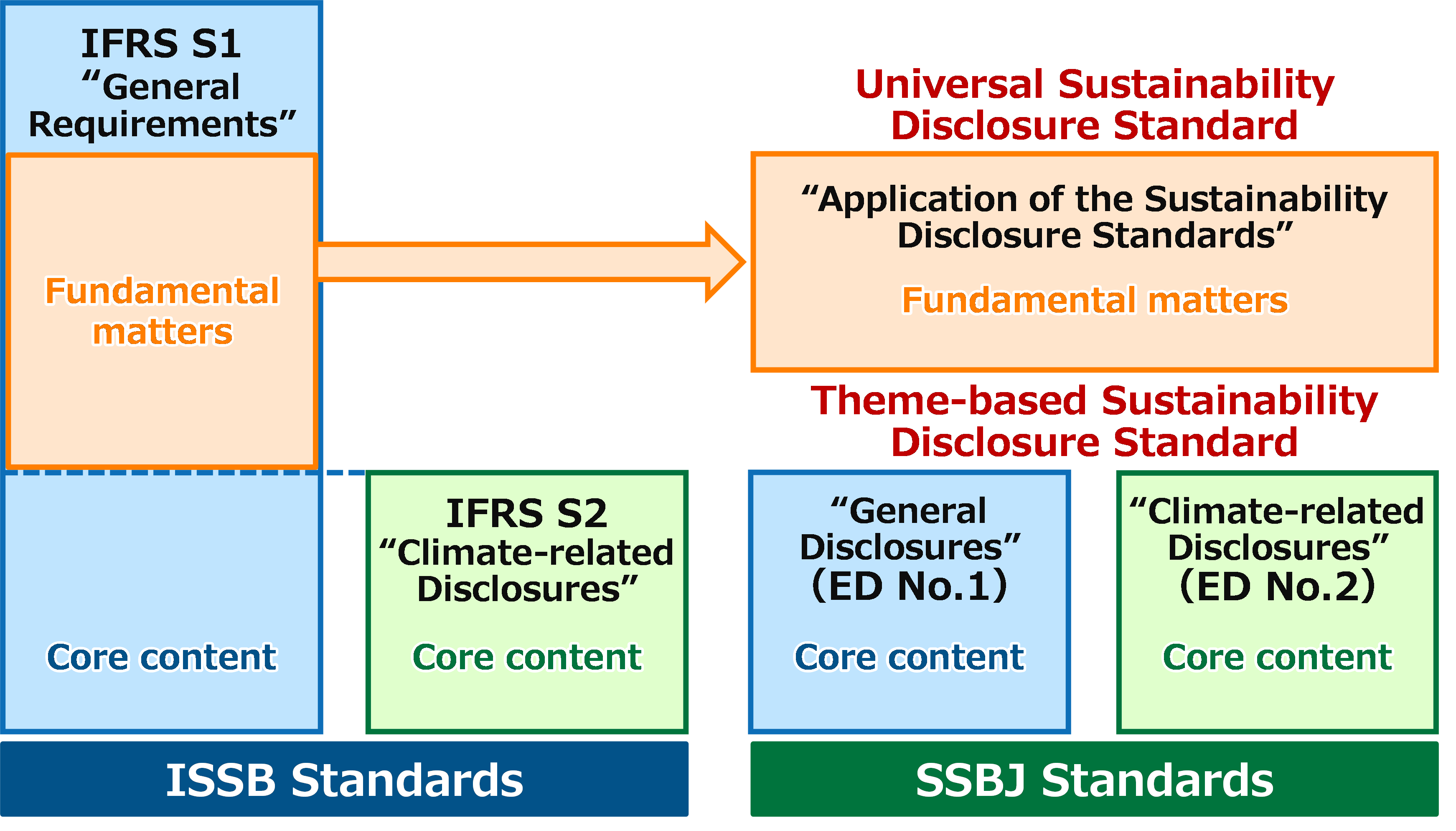

In developing high-quality and internationally consistent Sustainability Disclosure Standards, the SSBJ concluded that it would be useful for market participants to align the Japanese standards with the ISSB’s IFRS Sustainability Disclosure Standards. Accordingly, the SSBJ decided to incorporate all requirements in the IFRS Sustainability Disclosure Standards (IFRS S1 “General Requirements for Disclosure of Sustainability-related Financial Information” and IFRS S2 “Climate-related Disclosures”) and to add, when considered necessary, any jurisdiction-specific options the entity can choose to apply.

After extensive discussions, today, the SSBJ is pleased to announce the issuance of the following three Exposure Drafts of the Sustainability Disclosure Standards, which were approved for issuance at the 33rd Board Meeting on March 21, 2024:

1. Universal Sustainability Disclosure Standard Exposure Draft “Application of the Sustainability Disclosure Standards”

2. Theme-based Sustainability Disclosure Standard Exposure Draft No. 1 “General Disclosures”

3. Theme-based Sustainability Disclosure Standard Exposure Draft No. 2 “Climate-related Disclosures”

For the convenience of users of the standards, the standard corresponding to IFRS S1 was divided into two standards and issued separately. Specifically, the requirements of IFRS S1 other than those included in the “core content” section were included in the universal “Application of the Sustainability Disclosure Standards” standard, and the requirements in the “core content” section in IFRS S1 were included in the theme-based “General Disclosures” standard. The SSBJ thinks the division of IFRS S1 would not affect the resulting disclosures by entities, as all standards would need to be applied simultaneously.

The Exposure Drafts were developed under the assumption that the Sustainability Disclosure Standards issued by the SSBJ would eventually be required, under the Japanese securities laws and regulations, to be applied by companies listed on the Prime Market of the Tokyo Stock Exchange. The SSBJ is interested in hearing the views on the Exposure Drafts from those who are likely to be affected.

Yasunobu Kawanishi, Chair of the SSBJ stated:

“We would like to express our sincere gratitude to all those who have contributed to the development of the Exposure Drafts in such a short period of time. The Exposure Drafts incorporate all requirements in IFRS S1 and IFRS S2, with some additional jurisdiction-specific options the entity can choose to apply. We are interested in hearing the views from market participants, in particular, the need for such jurisdiction-specific options.”

The Exposure Drafts are available at:

https://www.ssb-j.jp/jp/domestic_standards/exposure_draft/y2024/2024-0329.html

The comment deadline is July 31, 2024.

The Exposure Drafts are published in the Japanese language only. Nevertheless, for the convenience of English speakers, the Secretariat of the SSBJ issued the summary of differences between the Exposure Drafts and the ISSB’s IFRS Sustainability Disclosure Standards in English language.

New! Summary of Differences between IFRS Sustainability Disclosure Standards and the SSBJ Exposure Drafts

New! Table of Concordance between IFRS Sustainability Disclosure Standards and the SSBJ Exposure Drafts

About the Sustainability Standards Board of Japan (SSBJ)

The Sustainability Standards Board of Japan (SSBJ) was established in July 2022 under the Financial Accounting Standards Foundation (FASF) and is a private-sector organization. The legal framework for sustainability disclosure standards is to be determined by the Financial Services Agency, and the SSBJ will develop domestic standards in line with such framework, once it is established. The SSBJ is a member of the Jurisdictional Working Group of the International Sustainability Standards Board (ISSB) and has been appointed as one of the inaugural members of the Sustainability Standards Advisory Forum (SSAF).

For more information about the SSBJ, visit its website at https://www.ssb-j.jp/en/